Over the past couple of months, market sentiment across the wholesale industrial, commercial and building supplies distribution sectors has been flush with a mix of commentary regarding recent business conditions.

Some distributors and manufacturers continue to tell us, “What slowdown?” in regards to economic noise of a pending industrial slowdown, pointing to March and April order numbers that set company records.

Others affirm that activity as at least started to cool after several years of post-pandemic.

This was perfectly illustrated in the 2023 First Quarter Baird-MDM Industrial Distribution Survey, which collected a plethora of interesting commentary from hundreds of distributors in industrial, commercial and building supply verticals. MDM Senior Editor Vesna Brajkovic conveniently collected it all in a May 12 Premium article here, and it’s also available in our MDM 1Q MarketPulse Report.

Beyond that, these mixed signals were also evident in the latest monthly wholesale trade data from the U.S. Census Bureau, which is packaged for MDM each month by Brian Lewandowski, Executive Director of the Business Research Division at the Leeds School of Business at the University of Colorado Boulder.

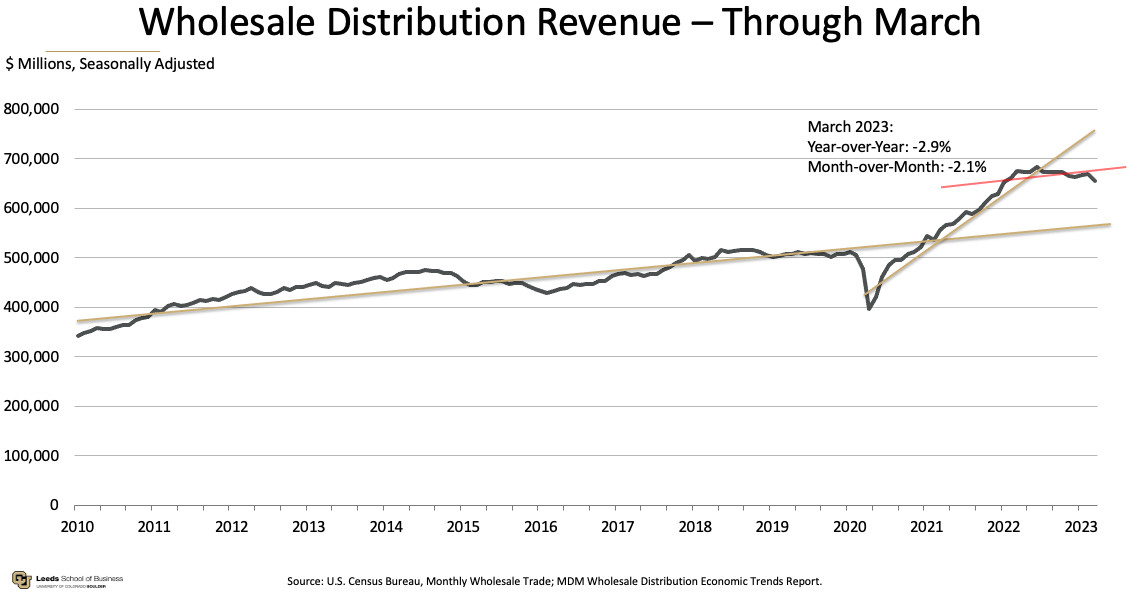

The Bureau’s data showed that the wholesale trade sector’s March revenue was down 2.9% year-over-year, and down 2.1% from February.

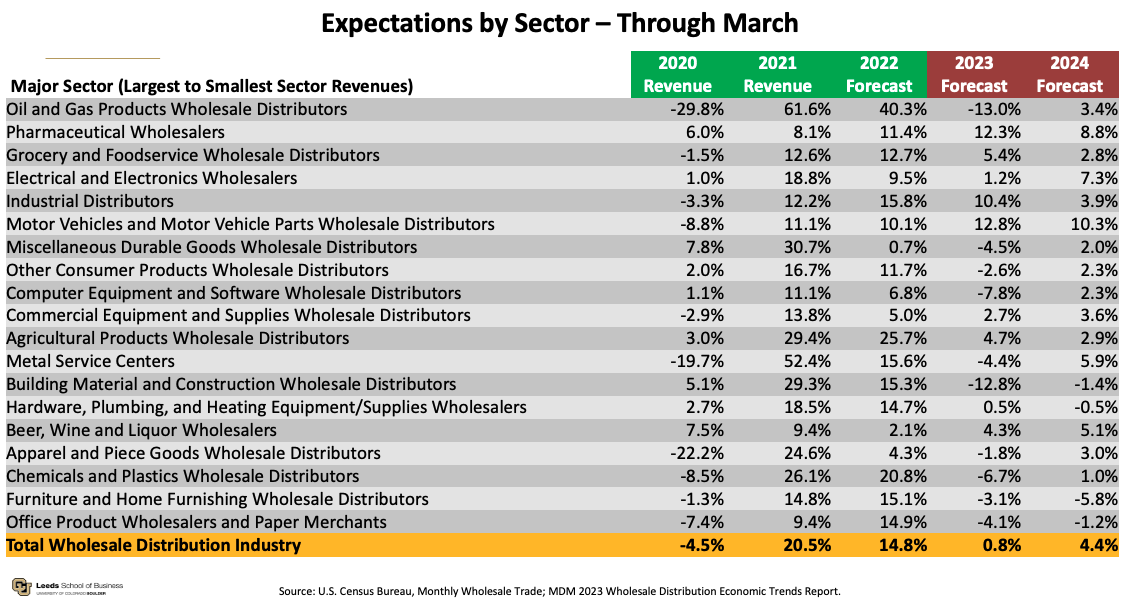

More granularly, only five wholesale sectors of the 19 the Bureau tracks that saw year-over-year revenue growth in March:

- Pharmaceutical: +16.2%

- Computer, Commercial and Medical Equipment: +12.5%

- Motor Vehicle Aftermarket Parts and Supplies: +9.3%

- Grocery & Foodservice: +4.9%

- Plumbing and HVAC: +0.9%

The other 14 sectors were all negative in March for year-over-year revenue, including:

- Electrical & Electronics: -2.1%

- Office Products & Paper: -4.0%

- Chemicals & Plastics: -5.7%

- Industrial Supplies: -7.8%

- Metal Service Centers: -14.1%

- Oil & Gas Products: -18.4%

- Building Materials: -18.5%

On a month-to-month basis, Pharmaceutical (+1.6%) and Furniture & Home Furnishings (+0.1%) were the only two sectors to see revenue growth in March.

Also on the pessimistic side, wholesale trade posted flat April employment growth vs. March — up 1.7% year-over-year.

At NAHAD’s 2023 annual conference April 26-May 2, ITR Economics’ Patrick Luce shared that his firm is forecasting U.S. GDP to slow to 0.9% full-year growth in 2023, following bumper years of 5.7% in 2021 and 2.1% in 2022. It’s then expected to fall to 0.3% decline in 2024 before rebounding to 2.5% growth in 2025, according to ITR.

Despite those near-term figures, distributors’ overall 2023 and 2024 full-year expectations actually improved in March compared to February. The Census Bureau’s monthly survey found that the total wholesale distribution industry forecasts 0.8% revenue growth for 2023 and 4.4% in 2024, up from 0.3% and 4.2% in February, respectively.

The sectors forecasting the most month-to-month optimistic growth in 2023 expectations were:

- Furniture & Home Furnishings: +2.2%

- Metal Service Centers: +1.8%

- Pharmaceutical: +1.7%

- Commercial Equipment & Supplies: +1.4%

- Chemicals and Plastics: +1.4%

- Motor Vehicles and Parts: +1.3%

- Grocery & Foodservice: +0.9%

- Industrial Supplies: +0.8%

- Office Products & Paper: +0.8%

The only sectors that moved more pessimistically in March were:

- Other Consumer Products: -2.1%

- Oil & Gas Products: -1.4%

- Hardware, Plumbing & Heating Equipment/Supplies: -0.1%

“Kind of a mixed bag,” Continental Portfolio Director Ryan Gaucher told me April 30 at NAHAD’s 2023 spring conference. “We still have a lot of distribution partners and other type of partners who see a strong future market ahead. We’re cautiously optimistic. We think there’s some opportunities where we’ll see increased growth opportunities, and others where we’ll see a bit of a slowdown.”

“Talking to some of our manufacturing partners, they’re starting to see a little bit of drop in distributor orders,” ARG Industrial President & CEO Mike Mortensen told me at NAHAD. “Some of us had been writing pretty big inventories going through the last year or so are starting to right size that a little bit, but demand still seems to be strong.”

You can find much more commentary regarding distributors’ near-term outlook in my resulting Podcast with NAHAD attendees, published May 10, and my April 26 Podcast that likewise gathered attendee voices from ISA23.

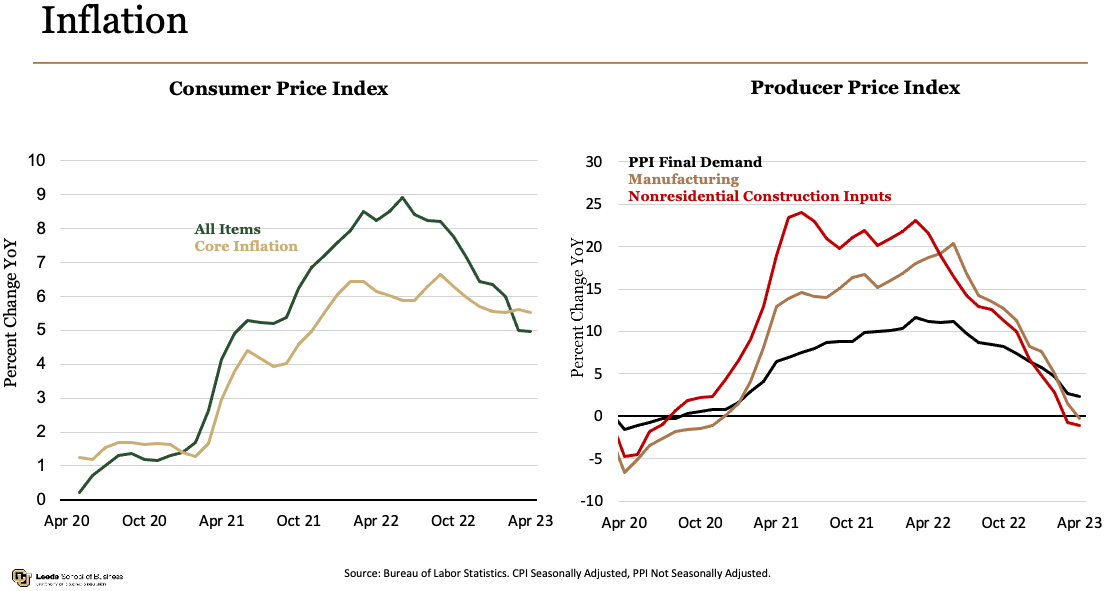

Below, find charts detailing April’s Consumer Price and Producer Price Indexes, along with a historic view of distributors’ revenue year-over-year revenue performance through March 2023.

Related Posts

-

Mike Hockett dives into the numbers for distributors’ 2023 expectations and the latest economic indicators…

-

While talks of a slowdown persist, industrial distributors outperformed nearly all other wholesale sectors in…

-

The group is expected to provide customers with services and solutions including comprehensive data center…