At the device level, new players into the market are ROHM, which recently introduced its EcoGaN portfolio with a first 150V device. Power Integrations, Navitas, Innoscience, EPC, and more,

“GaN fast chargers are growing rapidly in the handset market,” says Yole’s Taha Ayari, “since 2020, Yole has seen an increasing number of fast chargers featuring GaN devices from several players, like Power Integrations, Navitas, and GaN Systems. Now Innoscience is also contributing to this market with high volumes.”

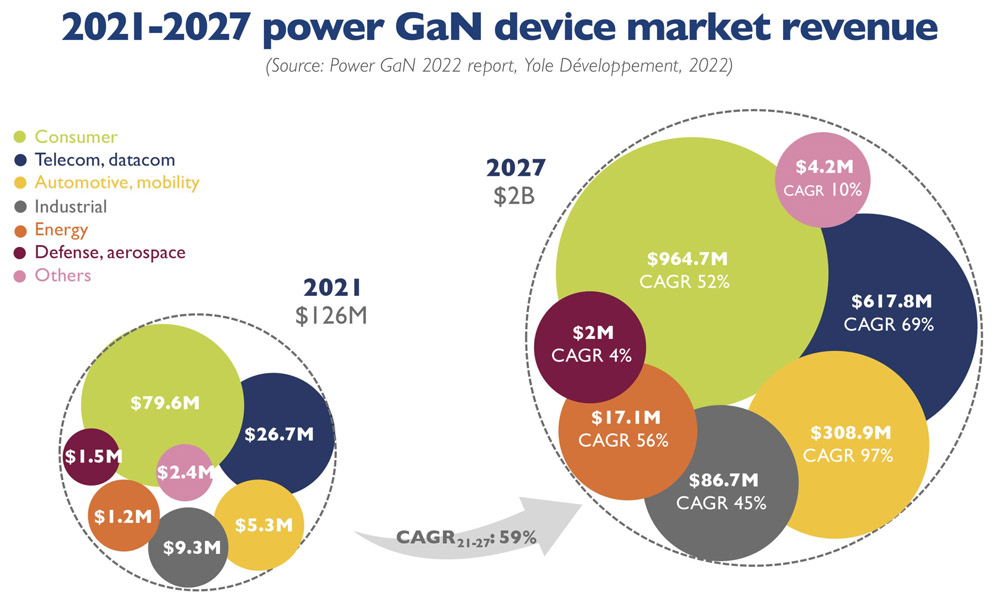

The consumer power supply market will be worth more than $915.6 million by 2027, with a 52% CAGR between 2021 and 2027. For datacom/telecom, Yole expects an increase in GaN penetration in the mid-term as regulations become stricter. The interest in adopting 48V-Point-Of-Load systems in data centers to reduce power consumption and cabling volume will favor GaN for low-voltage applications.

An increasing number of power suppliers are adopting GaN in their systems. Transphorm, EPC, Texas Instruments, Infineon, and GaN Systems have all announced several design wins. Therefore, the GaN market for datacom/telecom is expected to have a 69% CAGR over the forecast period, to more than US$617.8 million in 2027.

At a lower penetration level, automotive DC-DC converters and OBCs will be part of the next wave of growth during the forecast period. There are ever more collaborations between GaN device players, who are accelerating the automotive qualification of their products, and the Tier-1 and OEMs , who are evaluating automotive GaN solutions. The GaN automotive market is expected to exceed $227 million by 2027, with a 99% CAGR between 2021 and 2027.

Of the new players, Rohm is offering a 150V GaN product for telecom/datacom applications, BelGaN, a new GaN foundry based in Belgium, has recently acquired onsemi’s fab, and Navitas went public through a SPAC business combination after an agreement valued at $1.04 billion with Live Oak Acquisition Corp.

In China, the government has supported more investments from GaN players. It is noteworthy that Innoscience is investing more than $400 million to expand its 8-inch wafer capacity from 10k to 70k wafers per month by 2025.

A domestic supply chain for GaN power is well developed, especially for the consumer market. The transition to the 8-inch platform and the consolidation of the supply chain with more players at each level are driving lower manufacturing costs, especially at the epitaxy step, which constitutes the most significant part of a GaN device’s cost structure.

In fact, one of the big questions is around the use of in-house epitaxy and outsourced epitaxy for future high volumes.